Govt Targets ₹8.2 Lakh Crore Market Borrowing in H1 FY27, Keeps Fiscal Deficit at 4.3%

The Centre has outlined a detailed borrowing roadmap for the first half (H1) of FY 2026-27 April to September 2026 targeting ₹8.2 lakh crore through dated securities to finance its fiscal needs. This forms a significant portion of the government’s strategy to bridge the fiscal deficit estimated at ₹16.9 lakh crore , or 4.3% of GDP , reflecting a calibrated balance between growth spending and fiscal consolidation.

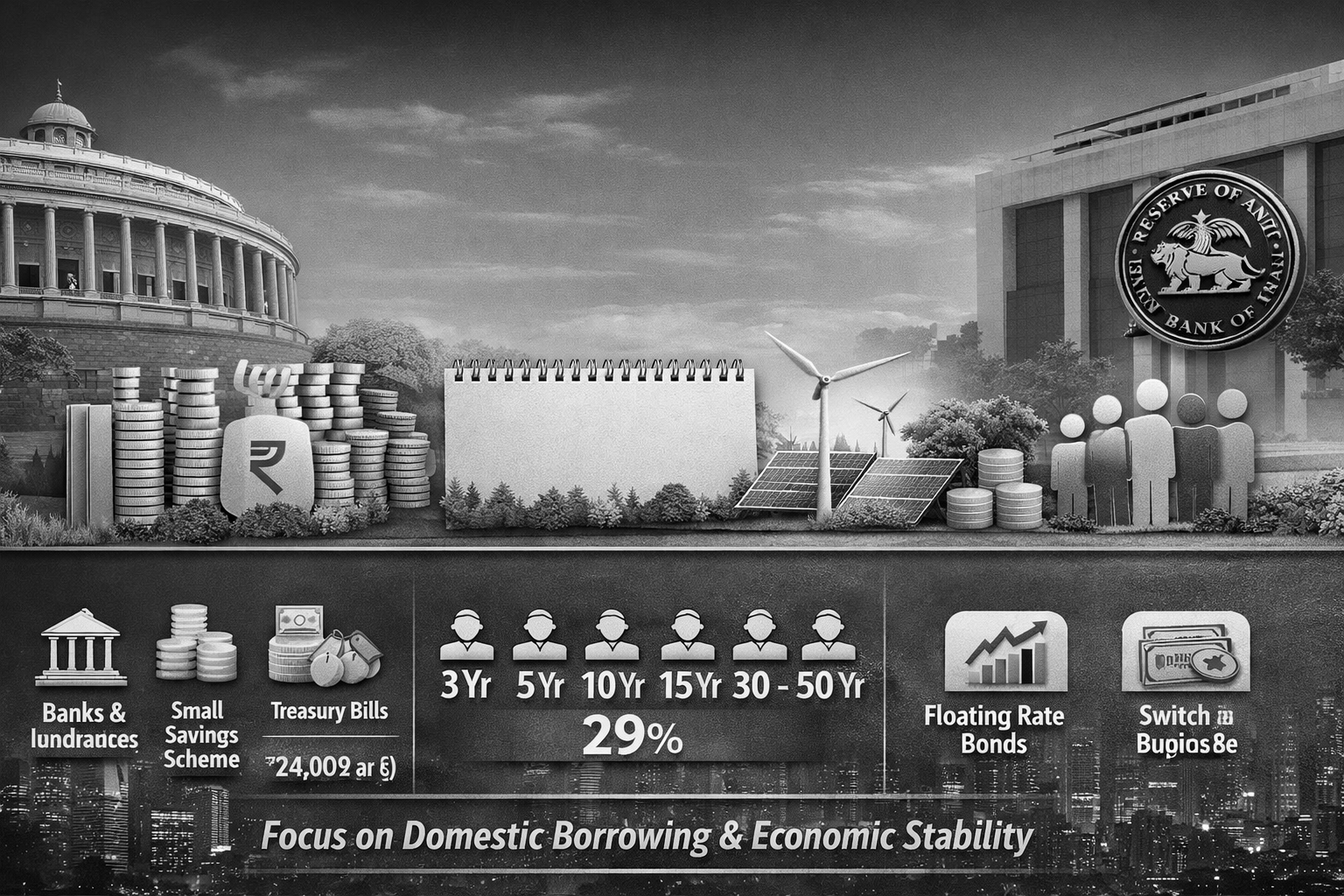

The gross market borrowing , initially budgeted at ₹17.2 lakh crore, has been revised to ₹16.09 lakh crore following switches of government securities aimed at managing redemption pressures. Of this, about 51% will be raised in H1 , with the government planning 26 weekly auctions , each ranging between ₹28,000 crore and ₹34,000 crore . The borrowing will span maturities from 3 years to 50 years , with 10-year bonds accounting for the largest share (29%) , indicating strong market preference for benchmark securities.

A key highlight of the borrowing plan is the inclusion of ₹15,000 crore in Sovereign Green Bonds (SGrBs) , reinforcing India’s push towards sustainable and climate-focused financing . To deepen market participation, the government has also reserved 5% of each auction for retail investors under the non-competitive bidding route, enhancing accessibility and transparency in the government securities market.

To fund its deficit, the Centre will rely predominantly on domestic investors , including banks, insurance companies, pension funds, and mutual funds , which form the backbone of demand for government securities. The Reserve Bank of India (RBI) will facilitate the borrowing programme by conducting auctions and ensuring adequate liquidity in the system. Additionally, a portion of the funding will come from small savings schemes such as PPF and NSC, which continue to provide a stable source of financing.

Notably, external institutions like the World Bank and Asian Development Bank play only a limited role , primarily funding specific development projects rather than contributing to routine fiscal deficit financing. India’s strategy of minimizing external borrowing helps reduce currency risks and vulnerability to global financial shocks , while maintaining macroeconomic stability.

The government has retained flexibility to adjust its borrowing calendar in response to evolving market conditions, including the option to issue floating rate bonds (FRBs) and inflation-indexed bonds (IIBs) . It will also continue monthly switch and buyback operations to smoothen the debt repayment profile and manage liabilities efficiently.

On the short-term front, the Centre plans to raise ₹24,000 crore weekly through Treasury Bills in the first quarter , while the RBI has set the Ways and Means Advances (WMA) limit at ₹2.5 lakh crore for H1 to manage temporary mismatches in government cash flows. The government also retains the greenshoe option of up to ₹2,000 crore per auction , allowing it to accept additional subscriptions based on demand.

Overall, the borrowing calendar reflects a well-structured fiscal strategy , anchored in high domestic mobilisation, controlled deficit levels, and market transparency . While the large borrowing programme could exert some pressure on interest rates and potentially crowd out private investment, it ensures steady funding for infrastructure, welfare programmes, and broader economic growth in the coming fiscal year.