Core Industries Dip 0.4% in March, Dragged by Fertilizers and Energy Weakness

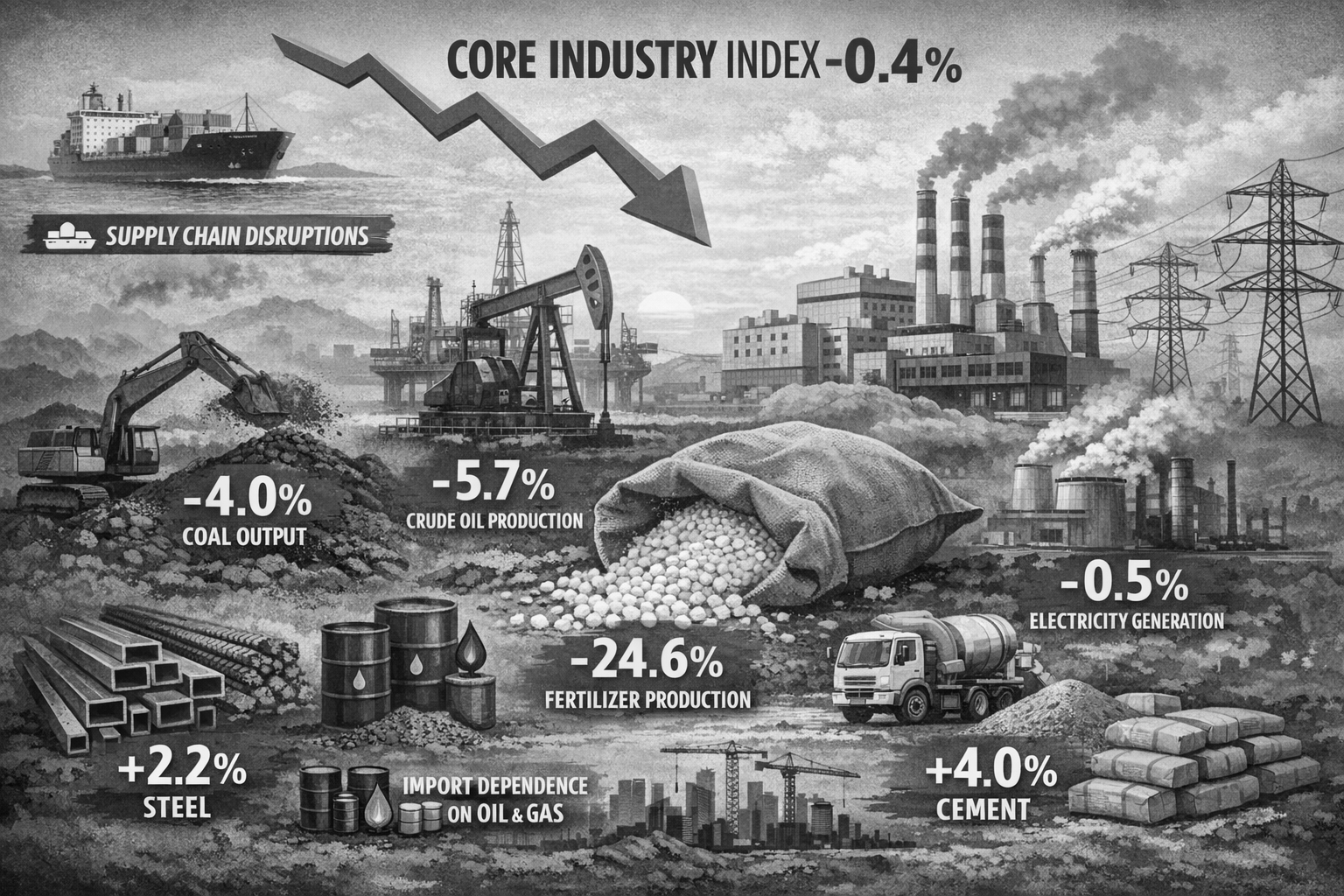

India’s core sector output slipped into contraction in March 2026, as the Index of Eight Core Industries (ICI) declined by 0.4% year-on-year , reversing the 2.8% growth recorded in February and signalling a late-year slowdown in industrial momentum. The eight key sectors Coal, Crude Oil, Natural Gas, Refinery Products, Fertilizers, Steel, Cement and Electricity together account for 40.27% of the Index of Industrial Production (IIP) , making them a crucial barometer of economic activity.

The contraction was largely driven by weakness in energy and input sectors, with Coal production (weight 10.33% ) falling by 4.0% , and Crude Oil (weight 8.98% ) declining by 5.7% in March. These declines reflect persistent structural issues such as ageing fields, limited domestic exploration, and high import dependence. The most severe drop was seen in the Fertilizers sector (weight 2.63% ), where output plunged by 24.6% , largely due to disruptions in the supply of key raw materials like natural gas and ammonia amid global geopolitical tensions. Meanwhile, Electricity generation (weight 19.85% ) declined by 0.5% , indicating both supply constraints and moderating demand.

Performance across the remaining sectors remained mixed. Natural Gas production (weight 6.88% ) grew by 6.4% in March, offering some support, though its cumulative output still declined by 2.8% during FY 2025–26. Petroleum Refinery Products (weight 28.04% ), the largest component, recorded marginal growth of 0.1% , with its cumulative output dipping by 0.1% , reflecting subdued refining activity amid volatile global crude markets.

In contrast, infrastructure-linked sectors continued to show resilience, highlighting sustained domestic demand. Steel production (weight 17.92% ) increased by 2.2% in March and recorded a strong 9.1% cumulative growth over the financial year, while Cement production (weight 5.37% ) rose by 4.0% in March with an 8.6% annual growth , supported by ongoing construction activity and government-led capital expenditure.

For the full financial year 2025–26 , the core sector posted a cumulative growth of 2.6% (provisional) , significantly lower than previous years, reflecting moderation in industrial expansion. The data underscores a structural imbalance, where energy and input sectors remain under pressure while infrastructure sectors continue to expand.

The March contraction highlights the combined impact of global and domestic challenges, including geopolitical disruptions affecting supply chains, rising input costs, and India’s heavy reliance on imports for crude oil and gas. These factors have constrained production across key sectors, outweighing gains from infrastructure activity. Overall, the slowdown appears largely supply-driven , with resilient demand in construction and investment unable to offset weaknesses in energy availability, making the near-term outlook dependent on stabilisation in global energy markets and improvements in domestic production capacity.